WEEKLY ECONOMIC UPDATE

Weekly Economic Update

Presented by Moorman, Harting Financial Services, Ltd.,

Market Recap – Week Ending Jan. 12

Stocks Mixed; Earnings, Retail Sales Data This Week

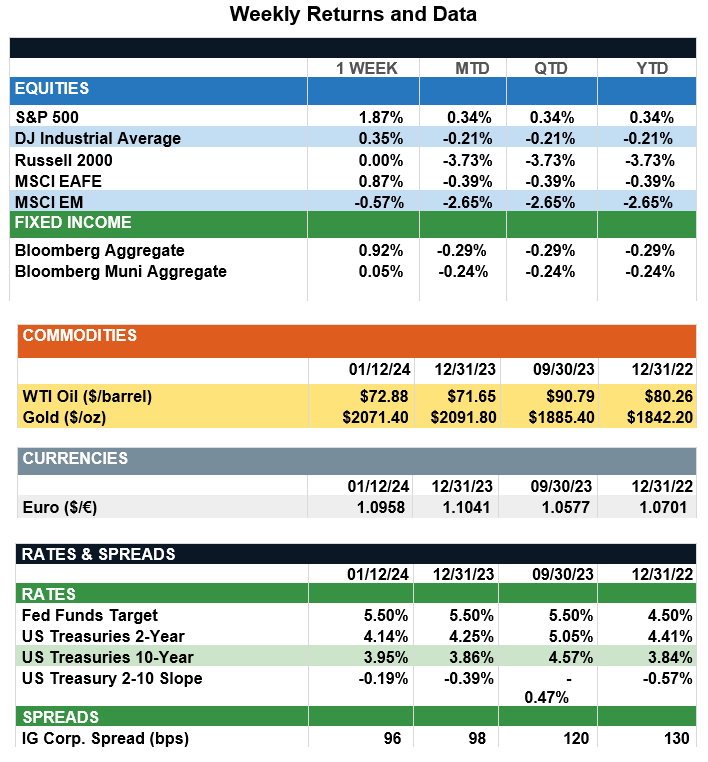

Overview: Stocks around the world were mixed last week as markets digested new inflation numbers and absorbed increasing geopolitical tensions. In the U.S., the S&P 500 index rose for the 10th of 11 weeks, finishing the week higher by 1.9% in the second trading week of the year. International developed stocks (MSCI EAFE) were higher as well, up 0.9%. Emerging market stocks (MSCI EM) were 0.6% lower on the week. The economic highlight in the U.S. was the consumer prices (CPI) report showing inflation increased more than expected, driven largely by shelter costs, car insurance and hospitality increases. Despite higher-than-expected inflation readings in December, futures markets still are pricing in about a 75% chance of a rate cut at the March 20 Fed meeting, and markets expect approximately six 0.25% cuts by the end of 2024. If realized, this would bring the funds rate to a range of 3.75%-4.00% at year-end. In the bond markets, yields fell on the expectation that inflation is expected to continue on a downward trend, with the 2-year and 10-year Treasury notes finishing the week at yields of 4.14% and 3.95%, respectively. Looking ahead, several major banks will release their earnings this week. Tuesday morning, both Morgan Stanley and Goldman Sachs reported profit and revenues above expectations. On the data front, retail sales are due out Wednesday, with month-over-month spending expected to increase 0.4% in December. Retail sales will be a key indicator for the health of consumer spending in economic growth expectations for the year ahead.

Update on Cash Products (from JP Morgan): Over the past two years, the Federal Reserve’s aggressive monetary tightening lifted short-term interest rates to their highest levels since the early 2000s. As a result, investors pounced on cash-like products for both safety and income in 2023, pushing money market fund assets to a record-high $5.98 trillion, and this number still is climbing. Of course, cash serves an important role in portfolios and yields above 5% look attractive. However, investors tempted by higher cash rates should remember re-investment risk is elevated, and holding too much cash can come at a cost. Looking across the last six rate-hiking cycles reveals cash tends to underperform both stocks and bonds in the year after rates peak. In fact, the S&P 500 and a balanced 60/40 stock-bond portfolio outperformed six-month CDs in five of the last six such periods, while the Bloomberg U.S. Aggregate outperformed across all six periods. Moreover, assuming peak rates for the current cycle already are behind us, cash is on pace to underperform once again. Since month-end CD rates peaked in September, the S&P 500 and U.S. Agg have experienced impressive gains of 12.1% and 6.5%, respectively, while a 6-month CD has returned a more modest 1.7% over the same period. Despite the recent market rally, investors have not missed their chance to move long-term money out of money market funds, and the opportunity cost of holding too much cash could increase further as the Fed eases policy in 2024. Given this, long-term investors should embrace opportunities across equities, fixed income and private markets to achieve their long-term goals.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.