WEEKLY ECONOMIC UPDATE

Market Recap – Week Ending April 12

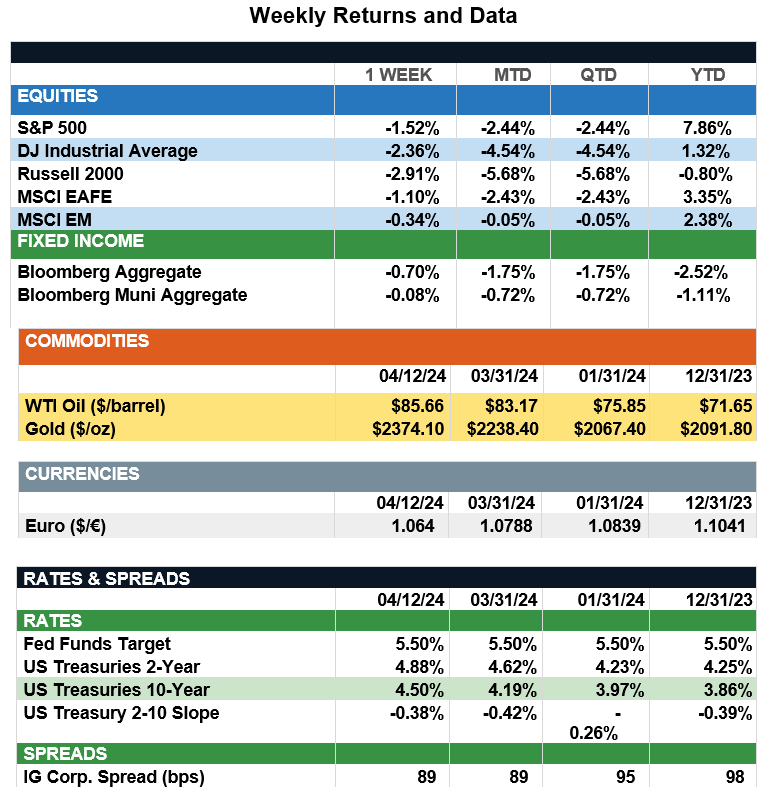

Stocks Falter After CPI Report; First-Quarter Earnings Reports Underway

Overview: U.S. stocks were in negative territory for the second consecutive week as the S&P 500 fell 1.5%, its worst week since October. International stocks outpaced domestic stocks with the MSCI EAFE falling 1.10%. Relative outperformance in both India and China helped buoy emerging markets stocks, with the MSCI EM index falling just 0.34% on the week. The big news for the week came in the form of an upside surprise in the U.S. Consumer Price Index (CPI), which rose 0.36% in March and 3.48% over the prior year. Sticky inflation remains a primary concern for the markets as the easing of monetary policy continues to get pushed further down the road. With six policy-setting meetings on the calendar for the FOMC for the remainder of this year, futures markets now are expecting just one or two 25bp rate cuts in 2024. The bond market has taken note, and yields across the curve continued to rise last week, with the yield on the 2-year and 10-year Treasury notes finishing the week around 4.88% and 4.50%, respectively. JPMorgan Chase, Citigroup, and Wells Fargo all kicked of first-quarter earnings results with strong revenues and earnings beats, boosted by healthy market returns and a strong U.S. economy. Still, guidance was cautious, noting several unknowns around interest rates and the economy.

Capital Gains and the Stock market (from JP Morgan): With Tax Day on April 15, it’s a good time to explore the relationship between the stock market and taxes and particularly how big capital gains tax payments may impact the stock market. Capital gains tax revenues tend to spike in fiscal years when the market undergoes significant sell-offs. In previous major market downturns, such as those in 2000, 2008 and 2022, it’s plausible that capital gains tax realizations could have intensified these sell-offs. One hallmark of a strong bull market is heavy trading as investors try to take advantage of a rising market or protect themselves against an impending correction. However, this trading results in the realization of significant capital gains, with taxes due by April of the following year. As investors fulfill their tax obligations, they often sell stocks to generate the necessary funds, leading to a drawdown in the market. This phenomenon likely played a contributing role in the sell-offs observed in 2000, 2008 and, to a lesser extent, 2022. However, this phenomenon may be less prevalent today, due to the more widespread use of low-turnover passive investments and tax-aware strategies. Because of this, capital gains taxes relative to the size of the market are expected to be lower this year compared to the peaks witnessed in the first decade of this century. While there are some similarities between the strong stock market surge of the last 18 months and tech bubble of the 1990s, the market’s vulnerability to capital gains tax payments probably isn’t one of them.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.